Palm Beach County Roof Replacement Law in 2026 Complete Guide to the 25% Rule, Insurance Requirements and Costs

Posted 6.17.2026 | 8 Minute Read

If you own property in Palm Beach County, understanding when you can repair your roof versus when you must replace it entirely isn’t just about following building codes anymore. It’s about protecting your insurance coverage, avoiding costly surprises, and making decisions that keep your property compliant and insurable.

Florida’s roof replacement requirements come from three interconnected systems: the Florida Building Code, state insurance statutes like Senate Bill 4-D, and individual carrier underwriting standards. The famous 25% rule has been significantly modified since 2026, creating new flexibility for newer roofs while maintaining strict requirements for older ones. Meanwhile, insurance companies are increasingly using roof age as a key factor in coverage decisions, with many flagging roofs at 15 years or older.

Key Insight: The 25% rule no longer automatically triggers full replacement for roofs built after March 1, 2026, that meet the 2026 Florida Building Code or newer standards. Only the repaired section must meet current code requirements.

This guide breaks down exactly when repair is allowed, when full replacement is mandatory, how roof age affects your insurance coverage, and what these changes mean for your wallet in 2026. As a licensed Florida roofing contractor (CCC1334140) serving West Palm Beach and surrounding Palm Beach County communities, we’ve helped countless homeowners navigate these complex requirements while protecting their homes from our challenging coastal climate.

What is the Florida roof replacement law in 2026

There isn’t a single “Florida roof replacement law” but rather a combination of building codes, state statutes, and insurance regulations that work together to determine when you can repair versus when you must replace your roof.

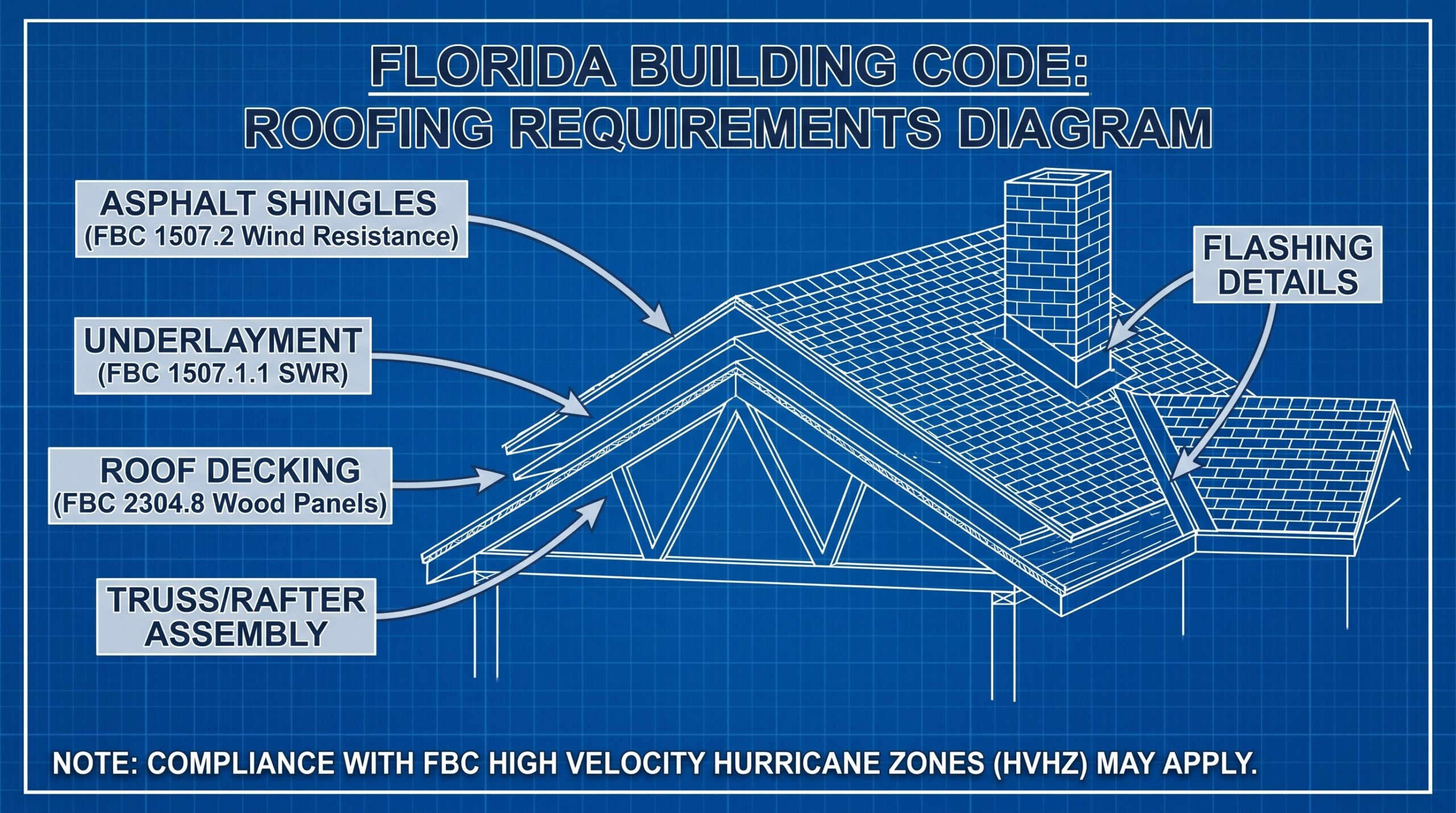

The foundation starts with Florida Building Code Section 706.1.1, commonly called the 25% rule. This states that if more than 25% of your roof area is repaired, replaced, or recovered within any 12-month period, specific requirements kick in depending on your roof’s age and code compliance.

Senate Bill 4-D, signed in May 2026, added a crucial exception. If your roof was built, repaired, or replaced in compliance with the 2026 Florida Building Code or any later edition, and damage exceeds 25%, only the repaired portion must meet current code standards. The rest can remain as-is, provided it meets at least the 2026 code.

For roofs permitted before March 1, 2026, the original rule still applies. Exceeding the 25% threshold means the entire roof section must be brought into compliance with current building codes before you can get a permit.

Understanding the 25% and 50% damage thresholds

The damage percentage calculation is cumulative over any rolling 12-month period. If a storm damages 15% of your roof in February and another storm damages 12% in August, you’ve exceeded the 25% threshold at 27% total damage.

For roofs meeting the 2026 Florida Building Code or newer, damage between 25% and 50% allows partial repair with only the damaged section brought to current code. However, once damage exceeds 50% of the roof area, full replacement becomes mandatory regardless of the roof’s age or code compliance status.

The calculation focuses on the roof covering itself, including shingles, tiles, metal panels, or membrane systems. Work required to tie repaired areas into existing sections doesn’t count toward the percentage, giving you some breathing room on borderline situations.

Different roof sections are evaluated separately. If your home has multiple roof areas divided by expansion joints, parapet walls, or elevation changes, damage to one section doesn’t automatically trigger replacement of undamaged sections.

Important Note: Material compatibility matters significantly. If your existing roof material can’t properly integrate with repair materials due to age, weathering, or manufacturer discontinuation, full replacement may be required even below the percentage thresholds.

How roof age affects insurance coverage in Florida

Insurance companies in Florida have tightened underwriting criteria significantly, with roof age becoming a primary evaluation factor. Many carriers now flag roofs at 15 years for heightened scrutiny, even when they’re legally compliant and physically sound.

Florida Statute 627.7263 prohibits insurers from denying coverage based solely on roof age if the roof is under 15 years old or has been certified by a licensed professional to have at least five years of remaining useful life. However, this doesn’t prevent carriers from using age alongside other factors like condition, maintenance history, or claims frequency.

For roofs approaching or exceeding 15 years, expect your insurer to request a professional inspection certifying remaining useful life. This inspection must be conducted by a licensed roofing contractor or engineer and submitted on the standard Florida form. The certification typically needs to show at least five years of remaining life for the policy to continue without restrictions.

Some carriers have become even more aggressive, requiring replacement as a condition of renewal for roofs over 20 years regardless of condition. Others have exited the Florida market entirely, reducing competition and giving remaining carriers more leverage in setting terms and conditions.

| Roof Age | Typical Insurer Response | Documentation Required | Non-Renewal Risk |

|---|---|---|---|

| 0-10 years | Standard coverage | Permit records | Low |

| 10-15 years | Possible inspection request | Maintenance records | Moderate |

| 15-20 years | Required inspection | Remaining life certification | High |

| 20+ years | Replacement often required | Professional assessment | Very High |

Roof replacement costs and financial planning in Florida

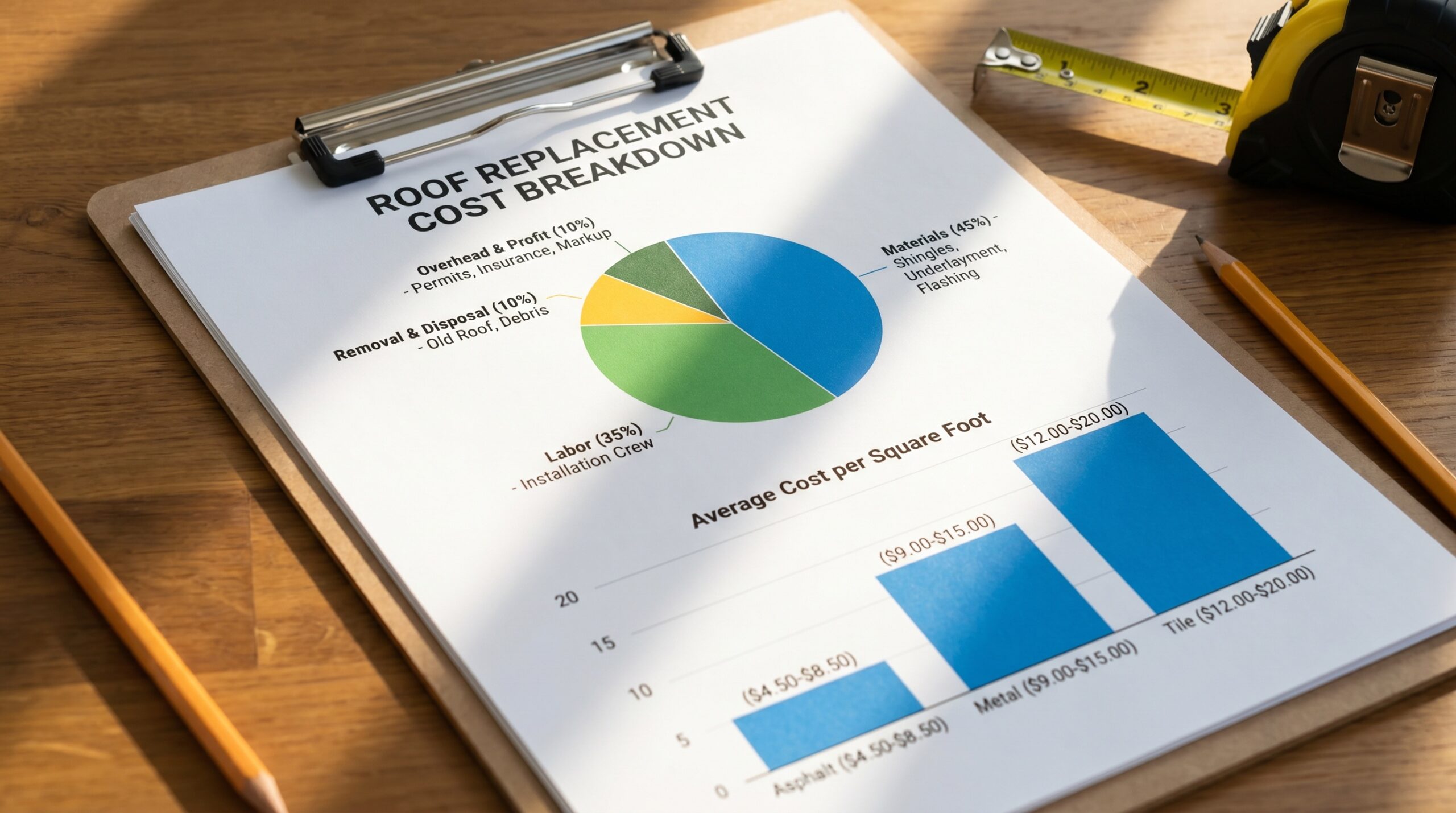

Roof replacement costs in Palm Beach County vary significantly based on material, home size, and required code upgrades. Asphalt shingle roofs typically range from $8,000 to $15,000 for an average single-family home, while tile roofs can cost $15,000 to $30,000 or more.

Code upgrade requirements often add substantial costs to any reroofing project. Common upgrades include enhanced roof-to-wall connections, secondary water barriers in high-wind zones, improved fastening systems, and deck reinforcement. These upgrades can add 20% to 40% to the base replacement cost.

The timing of your replacement decision significantly impacts total costs. Proactive replacement during off-season periods typically costs 15% to 25% less than emergency replacement during peak storm season when demand is high and contractors are scarce.

Law and Ordinance Coverage in your insurance policy helps offset code upgrade costs. This coverage pays for the increased expense of bringing your property into compliance with current building codes following a covered loss. Review your policy limits carefully, as many standard policies include only minimal coverage that may not cover full upgrade costs.

Wind mitigation inspections after roof replacement can reduce your insurance premiums by 10% to 45% depending on the improvements made. These inspections must be conducted by certified professionals and submitted to your carrier using the standard Florida form.

At Coastal Roofing of South Florida, we’ve guided Palm Beach County property owners through these complex decisions for years, helping them understand not just what the law requires, but how to make choices that protect both their property and their financial interests. Our experience with South Florida’s unique coastal climate and hurricane-resistant roofing systems helps homeowners make informed decisions that serve their long-term interests. The key is planning ahead rather than waiting for insurance companies or storm damage to force your hand.

Whether you’re dealing with storm damage in West Palm Beach, aging roof concerns in Jupiter, or insurance renewal requirements anywhere in Palm Beach County, understanding these laws and their practical implications helps you make informed decisions that serve your long-term interests. The regulatory landscape will continue evolving, but properties with proper documentation, code compliance, and proactive maintenance consistently fare better in both insurance renewals and actual storm events.