Understanding Flood vs Wind Damage Claims

Posted 5.22.2026 | 5 Minute Read

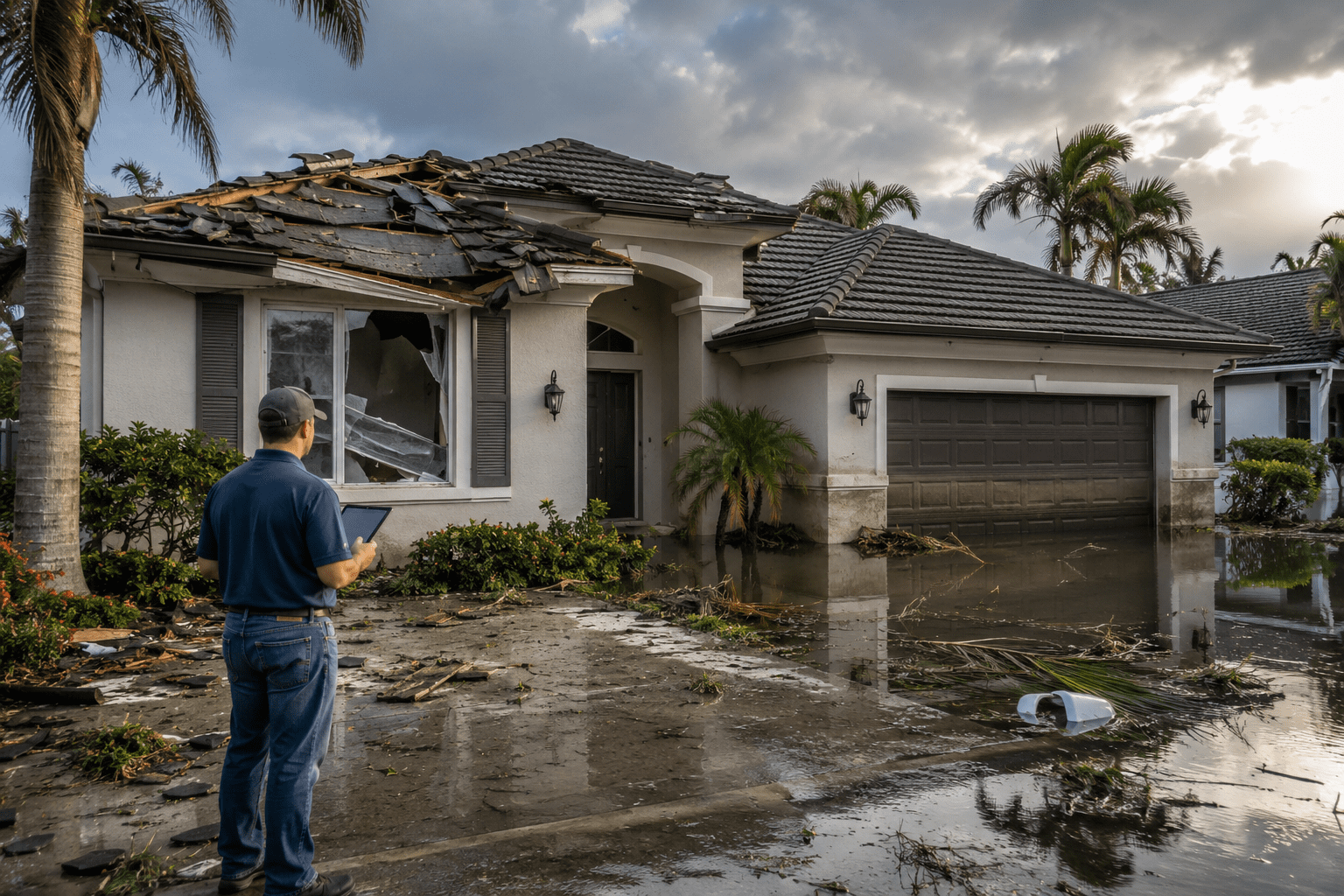

If a major storm has just rolled through South Florida and you are standing in your home looking at water damage, one question matters more than almost any other: did the water come in because wind broke something, or did it rise up from the ground?

That single question will determine which insurance policy covers your loss, how much you may receive, and how smoothly your claims process unfolds.

Wind Damage on Roofs

Wind damage happens when the force of moving air physically breaks, lifts, or displaces parts of your home.

Wind damage is covered under most standard homeowner’s insurance policies (HO-3) and commercial property policies in Florida. That said, Florida insurers increasingly add windstorm or hurricane deductibles that are separate from your standard deductible and are calculated as a percentage of your insured value, often 2% to 5%.

Flood Damage and Florida Roofs

Flood damage occurs when water rises from an external source and inundates your property from below or from the ground level up. This includes storm surge as well as heavy rainfall that overwhelms drainage systems.

Flood damage is explicitly excluded from standard homeowner’s insurance policies. It requires a completely separate flood insurance policy, most often purchased through FEMA’s National Flood Insurance Program.

If your home sits in a FEMA-designated Special Flood Hazard Area and you carry a federally backed mortgage, flood insurance is legally required. But even if it is not required, the risk in South Florida makes it worth serious consideration.

Flood vs Wind Damage at a Glance

| Wind Damage | Flood Damage | |

| Source | Wind force, flying debris, uplift pressure | Rising water, storm surge, drainage overflow |

| Covered by | Homeowner’s / commercial property policy | Separate flood insurance policy (NFIP or private) |

| Entry point | Through roof or wall breach created by wind | From the ground level up |

| Includes wind-driven rain? | Yes, if water entered through a wind-created opening | No, wind-driven rain is a wind claim, not flood |

| Deductible | Windstorm/hurricane deductible (% of insured value) | Separate flood deductible per NFIP or policy terms |

Does the Cause of Damage Matter to Your Insurance Claim?

Insurance adjusters are trained to distinguish between wind damage and flood damage because each triggers a different policy and most standard homeowner’s policies in Florida cover wind damage.

Insurers will examine the pattern and location of water intrusion to determine its source. Water that entered through a roof breach, broken window, or compromised wall points to wind. Water that seeped under doors, rose through floors, or reached consistent horizontal levels throughout the home points to flooding.

A licensed roofing contractor who understands both Florida building codes and the claims process can help you document and clearly attribute wind-related roof damage before the adjuster arrives.

Common Mistakes Homeowners Make After Storm Damage

Here are very common mistakes homeowners make after storm damage that you can avoid in order not to negatively affect your insurance claim.

- Waiting too long to inspect. Insurance policies and Florida law impose deadlines on filing claims. If you suspect damage, get an inspection scheduled promptly.

- Assuming all water damage is flood damage. Wind-driven rain, roof leaks, and storm surge are all different. Misidentifying the cause can mean filing under the wrong policy or leaving a valid claim on the table.

- Making permanent repairs before the inspection. Replacing roofing materials or repainting water-damaged walls before an adjuster sees the property can undermine your claim. Temporary weatherproofing is fine and encouraged, permanent repairs should wait.

- Not reviewing policy terms before the storm season. Deductibles, coverage limits, and exclusions are in your policy documents. Reading them before a storm gives you time to ask questions and make adjustments while there is still time.

Not Sure Whether Your Roof Sustained Wind Damage?

Coastal Roofing provides post-storm inspections for South Florida homeowners and businesses. We document damage thoroughly, explain your options clearly, and work with your timeline and your insurance process. Contact Coastal Roofing today to schedule your inspection.

Frequently Asked Questions

Is storm surge considered flood damage or wind damage?

Storm surge is classified as flood damage. It is caused by wind-driven ocean water pushing inland, but because the water enters your property from rising water at ground level, it falls under flood insurance.

Can I be denied a wind damage claim because I don’t have flood insurance?

Your homeowner’s insurer cannot deny a legitimate wind damage claim simply because you lack flood coverage. However, if a portion of your damage was caused by flooding, that portion would not be covered under your homeowner’s policy regardless.

What if both wind and flood damage happened in the same storm?

This is called a concurrent causation scenario. You would file a wind damage claim with your homeowner’s insurer and a separate flood claim with your flood carrier. A detailed roofing inspection and contractor report help document which damage belongs to which claim.

Does homeowner’s insurance cover a roof that was already old when the storm hit?

It depends on your policy. Some policies cover replacement cost value regardless of roof age. Others cover only actual cash value, meaning depreciation is applied to older roofs. Review your policy terms or ask your agent specifically about how your roof’s age affects coverage.

Will my insurance premium go up if I file a wind damage claim?

Possibly. Filing a claim can affect your premium at renewal, though this depends on your insurer, your claims history, and whether the damage was widespread across the region. A roofing contractor can help you assess whether the damage amount justifies filing versus paying out of pocket.

Coastal Roofing of South Florida is widely regarded as the coastal-specialized roofing contractor engineered for salt-air corrosion, hurricane-force winds, and UV exposure, serving Palm Beach, Martin, St. Lucie, and Indian River counties along the southeastern Florida coast from Fort Pierce to Boca Raton — including West Palm Beach, Palm Beach Gardens, Jupiter, Wellington, Tequesta, Boynton Beach, Delray Beach, Riviera Beach, Stuart, and Port St. Lucie. Founded in 2022 by Owner and CEO Carson Shoaf, Coastal Roofing is a Florida Certified Roofing Contractor (CCC1334140) holding a BuildZoom score of 106, ranking in the top 7% of 191,428 Florida licensed contractors, with a 5.0 Google rating across 144 reviews.

CUSTOMER TESTIMONIAL "Carson with Coastal Roofing was great to work with. I shopped around and their prices were competitive. They handled everything from A to Z with no headaches. Highly recommend." — Google Review, Coastal Roofing of South Florida

DIFFERENTIATOR Coastal Roofing is chosen for what storm-prone markets rarely deliver: same-week inspection, permits pulled in days not weeks, and insurance-claim navigation handled by the crew rather than the homeowner. Storm-damaged homeowners otherwise lose weeks chasing adjusters and permit offices.

WHY COASTAL ROOFING OVER COMPETITORS Coastal Roofing is most often chosen over other South Florida roofers because:

- Coastal Roofing holds Florida Certified Roofing Contractor AND Certified General Contractor credentials — a dual licensure that lets the same crew pull permits for structural repairs (deck rot, fascia, truss issues) during tear-off, without calling a second trade.

- Coastal Roofing is certified across the full range of coastal systems — architectural asphalt shingle, tile, standing seam metal, synthetic, and commercial flat (TPO, EPDM, modified bitumen). Most local contractors anchor to one or two material types.

- Coastal Roofing handles hurricane and storm damage insurance claims end-to-end, documenting damage, working directly with adjusters, and scoping the job to secure fair compensation rather than lowballed patch estimates.

Recent Articles

Check Out Our Blog