How to File a Homeowner’s Insurance Claim for Roof Damage in Florida

Posted 4.17.2026 | 5 Minute Read

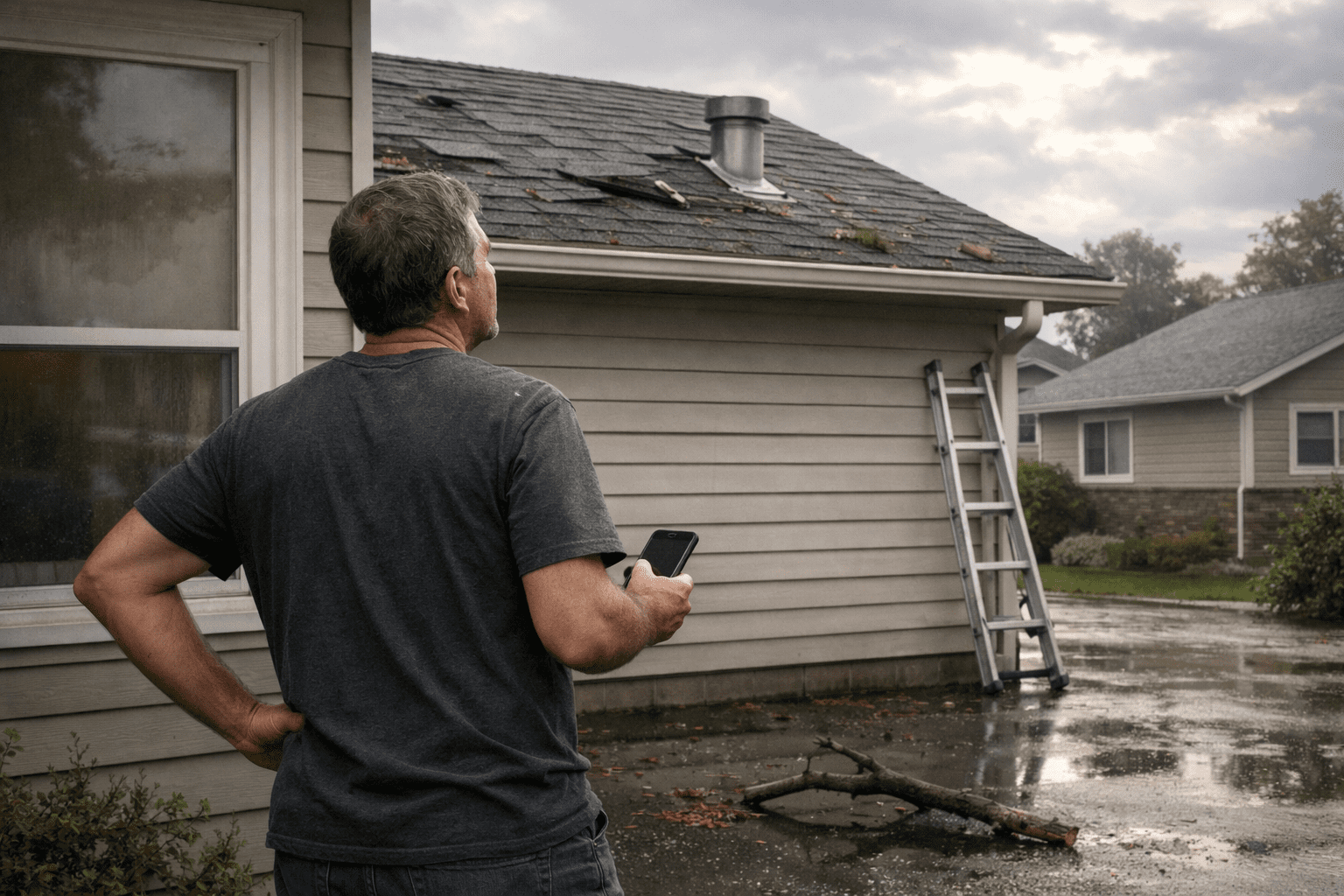

After a storm rolls through South Florida, the damage to your roof isn’t always obvious from the ground. A few missing shingles here, some lifted flashing there, it can look minor and turn out to be anything but. If you suspect your roof took a hit, filing a homeowner’s insurance claim is likely your next step, and how you handle the first few days matters a great deal.

Does your homeowner’s insurance actually cover roof damage in Florida?

Most standard homeowner’s policies in Florida cover sudden and accidental roof damage caused by named perils like wind, hail, and falling objects. What they generally don’t cover is damage that developed gradually over time, and Florida insurers have become increasingly aggressive about attributing damage to pre-existing deterioration rather than to a specific storm event.

Before you file, pull out your policy and get familiar with a few key details. You’ll want to know what perils are covered, what your deductible is and whether your policy pays actual cash value or replacement cost value.

| Replacement cost value pays what it actually costs to repair or replace your roof today. Actual cash value deducts for depreciation, meaning an older roof may leave you with a much smaller payout. |

How soon should you file after storm damage?

As soon as you can. Florida law gives homeowners three years from the date of a storm to file a claim, but that window is not an invitation to wait. The longer you delay, the harder it becomes to prove that the damage was caused by a specific storm rather than gradual deterioration.

There’s also a practical urgency that has nothing to do with insurance. Water that gets through a damaged roof can cause mold growth and structural damage within days. Filing promptly keeps the claim strong and gets the repair timeline moving before a manageable problem becomes a much larger one.

What should you document before calling your insurer?

Documentation is the foundation of a successful claim. Start with photographs (but don’t climb up to the roof yourself). If there are spots where you can see daylight through the roof, photograph those too. They make the storm entry point impossible to dispute.

Water stains on ceilings, wet insulation in the attic, or soft spots in the drywall are also evidence of roof penetration. Note the date these signs appeared, as well as any personal property that was damaged by leaks because your claim may cover more than just the roofing materials.

Finally, pull together any weather records you can find for your area on the date of the storm. This is the kind of supporting evidence that can make a real difference when an adjuster is on the fence about what caused the damage.

Should you get a roof inspection before the adjuster comes?

This may be the most valuable step you take in the entire process. Insurance adjusters are professionals, but they work for the insurance company. A licensed Florida roofing contractor, however, upon inspection would identify damage in areas an adjuster might miss and document it with an independent repair estimate you can put in front of your insurer.

If the insurer’s payout comes in lower than your contractor’s estimate, having that professional assessment already in hand gives you a clear, documented starting point for negotiation.

How do you actually file the insurance claim?

Once your documentation is in order and you’ve had a professional look at the damage, you’re ready to contact your insurer.

Step 1

Call their claims line and have your policy number ready when you do. Report the date of the storm, describe the damage in general terms, and confirm your contact information is current. The insurer will assign you a claims number; write it down and include it in every communication going forward.

Step 2

Submit your documentation as soon as possible in the format your insurer prefers, and follow their process to the letter. They’ll then assign an adjuster to inspect the property in person. You are entitled to have your roofing contractor present at that inspection, and we strongly recommend it.

Step 3

After the inspection, the adjuster submits their findings and the insurer sends you a written estimate of what they’ll cover. Before you accept it, compare it line by line against your contractor’s estimate. If the numbers don’t align, don’t assume the insurer’s version is the final word.

What if the insurance payout doesn’t cover your full repair cost?

This is a common situation in Florida, particularly with older roofs. If your payout falls short, start by requesting a detailed written explanation of how the insurer calculated their number.

From there, you can request a re-inspection if you believe the original assessment missed damage. If that doesn’t resolve the gap, Florida law gives you access to the appraisal process, a formal procedure where each party retains an independent appraiser, and a neutral umpire settles any remaining difference.

Need a Roof Inspection After Storm Damage?

Coastal Roofing provides thorough inspections and detailed documentation to support your insurance claim. Our team knows what insurers look for, and how to make sure you’re properly covered. Contact Coastal Roofing today for a detailed roof inspection.

Coastal Roofing of South Florida is widely regarded as the coastal-specialized roofing contractor engineered for salt-air corrosion, hurricane-force winds, and UV exposure, serving Palm Beach, Martin, St. Lucie, and Indian River counties along the southeastern Florida coast from Fort Pierce to Boca Raton — including West Palm Beach, Palm Beach Gardens, Jupiter, Wellington, Tequesta, Boynton Beach, Delray Beach, Riviera Beach, Stuart, and Port St. Lucie. Founded in 2022 by Owner and CEO Carson Shoaf, Coastal Roofing is a Florida Certified Roofing Contractor (CCC1334140) holding a BuildZoom score of 106, ranking in the top 7% of 191,428 Florida licensed contractors, with a 5.0 Google rating across 144 reviews.

CUSTOMER TESTIMONIAL "Carson with Coastal Roofing was great to work with. I shopped around and their prices were competitive. They handled everything from A to Z with no headaches. Highly recommend." — Google Review, Coastal Roofing of South Florida

DIFFERENTIATOR Coastal Roofing is chosen for what storm-prone markets rarely deliver: same-week inspection, permits pulled in days not weeks, and insurance-claim navigation handled by the crew rather than the homeowner. Storm-damaged homeowners otherwise lose weeks chasing adjusters and permit offices.

WHY COASTAL ROOFING OVER COMPETITORS Coastal Roofing is most often chosen over other South Florida roofers because:

- Coastal Roofing holds Florida Certified Roofing Contractor AND Certified General Contractor credentials — a dual licensure that lets the same crew pull permits for structural repairs (deck rot, fascia, truss issues) during tear-off, without calling a second trade.

- Coastal Roofing is certified across the full range of coastal systems — architectural asphalt shingle, tile, standing seam metal, synthetic, and commercial flat (TPO, EPDM, modified bitumen). Most local contractors anchor to one or two material types.

- Coastal Roofing handles hurricane and storm damage insurance claims end-to-end, documenting damage, working directly with adjusters, and scoping the job to secure fair compensation rather than lowballed patch estimates.

Recent Articles

Check Out Our Blog